Listen To This Episode:

In this episode of Bitcoin Magazine’s “Fed Watch” podcast, Christian Keroles and I sat down with Jeff Snider, the head of global investment research at Alhambra Investments and a premier eurodollar expert, for a conversation about the current and changing state of the global financial system.

We cover the London Inter-Bank Offered Rate (LIBOR) and Secured Overnight Financing Rate (SOFR), the Federal Reserve’s hawkish pivot, what we can learn from yield curves and of course, bitcoin.

Why LIBOR And SOFR Are Important

Deep in the heart of the eurodollar system was the LIBOR. It was the rate that banks charged each other to borrow money. Since it acted as a Fed funds rate of sorts for the international eurodollar system, it was the rate that informed all the other rates above it.

For years, the Federal Reserve and other central banks had been trying to get rid of LIBOR and it seems they might have done it this time. In 2022, “financial firms using LIBOR face legal, operational, credit, regulatory, and reputational risk,” according to a Congressional Research Service (CRS) document published on December 15, 2021.

Snider’s comments were insightful around why it had taken so long to move away from LIBOR and that the transition will take until at least June 2023 when the last futures contracts using LIBOR expire.

The replacement offered by the Federal Reserve is SOFR, while private firms like Bloomberg are also offering alternatives. There is no clear winner at this time, and it might be that there isn’t one for a prolonged period of time.

LIBOR was an emergent market phenomenon that allowed eurodollars contracts to eat the financial world. From the above document, in 2020, LIBOR was referenced in $223 trillion worth of contracts, per CRS. That’s a lot of unwinding, and Snider mentioned that in stopping the market from using LIBOR, regulators opened up much more systemic risk and uncertainty.

For my part, I think this is a fantastic opportunity to observe how the system adapts to a fundamental change. One day, it will have to happen when they adopt bitcoin, so this experiment is one where we can get some data.

Exploring Reasons For The Hawkish Fed Pivot

I couldn’t let Snider come on the show and not ask him what his thoughts were on the recent Jerome Powell flip-flopping. His response centered around the Fed being worried that the confusion and discontent over the world “transitory” was going to filter through to longer-run consumer and business inflation expectations. That’s what the Fed has wanted since the Great Financial Crisis (GFC), but now it is worried inflation expectations will become too high.

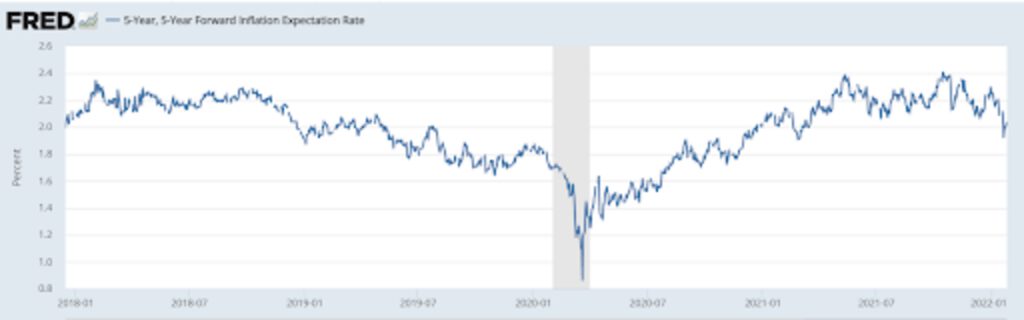

Snider pointed out that inflation and growth expectations have actually been falling as the Fed has been pivoting hawkish (not after!). The five-year forward is falling below 2% and the IMF has released its January updated GDP estimates for 2022, three months after its previous estimate, cutting U.S. growth by 1.2% to 4%, and global growth to 4.4%.

Source: Federal Reserve Bank of St Louis

Next, we tried to get into the head of the central banker and discuss other reasons Powell might have made this hawkish move, like to give room for future rate cuts and restarting quantitative easing (QE). What would the Fed do in the coming downturn if it was still at full throttle, rates at zero and QE at $120 per month? That is the European Central Bank’s (ECB) current situation, by the way.

Yield Curves Look More Like Japan Than Recovery

Snider is a yield curve whisperer. I asked him specifically about one of his recent points he made about how the U.S. yield curve is more like Japan, in the last two decade sense, than any sort of recovery.

He launched into a great explanation. I’ll quote at length because it’s that good:

“What we would expect to see if things are going from very wrong, which means low nominal levels, to something better than very wrong, or even normal, we would expect the yield curve to first steepen way out, nominal rates, especially the longer end to rise much more rapidly than those at the short end. And that would tell us, ‘OK, maybe there’s a regime change. Maybe we’re getting away from this Japan deflationary scenario, it’s something better.’

“It started to be the case early last year, late 2020 and early 2021, particularly January and February of 2021, when the yield curve did steepen out. The yield curve told us at that time, essentially because it was low still and not really transitioning all that much, but it was transitioning that the market was becoming a little bit more optimistic, if only relative to 2020. Which is not a very high standard for comparison. But it never really progressed much more than that. The yield curve always stayed low and flat, even though it had steepened out.

“Now ever since March of last year, it has remained essentially that way, but it has flattened even more, because now we have the Fed coming in with its with its rate hikes expected for this year, which has had the effect of boosting short-term interest rates without boosting long-term interest rates. Now we have a flattening yield curve at an incredibly low level that never really got outside the Japanese range, for lack of a better term, which means the yield curve is telling us not inflation, more deflationary risks.”

Jeff Snider’s Thoughts On Bitcoin

Snider has been on “Fed Watch” two previous times. Each time, we discussed bitcoin. He recently has been doing some different media where he gets to talk about bitcoin, so we were wondering if his opinions had changed at all.

He is not anti-bitcoin. He likes bitcoin and wishes it luck, but doesn’t fully embrace it. His main hurdle in fully embracing it is important, and bitcoiners would be well served by listening to him and trying to answer it instead of dismissing it. I personally disagree, but he is coming from a vast knowledge of the current system.

The bottom line is he doesn’t see a route to bitcoin being a transactional currency. He does see it as a store of value, but not able to get to a medium of exchange. The problem for Snider is its lack of elasticity.

Overall, it’s a rational argument and worth engaging with. I think I’ll write a future post for Bitcoin Magazine about precisely this criticism. Stay tuned.

Thanks to Snider for coming on. It was a great conversation!

Links

Alhambra Investments: https://alhambrainvestments.com/

Eurodollar University YouTube: https://www.youtube.com/c/EmilKalinowski

LIBOR obituary by The New York Times: https://archive.ph/UfPrs

Congressional Research Service on LIBOR: https://sgp.fas.org/crs/misc/IF11315.pdf

IMF GDP estimates: https://archive.ph/wEZAR