The sudden crash

Back in April 2022, Terra was still a public chain with a market cap of $41 billion and plenty of rosy visions. However, in just one month, its native algorithmic stablecoin UST de-pegged from the dollar due to manipulation by big institutions and flawed mechanisms. As a result, Terra’s market cap plummeted from $41 billion to $1.2 billion (as of May 17), a 97% drop. After UST lost its peg, its TVL also collapsed, dropping from $21 billion to $300 million in just one week. No egg stays unbroken when the nest is overturned. As UST de-pegged from the dollar, the TVL of projects backed by the enabling ecosystem of Terra in the past fell from $21 billion to $300 million within a week. How will the Terra-powered projects find a way out? Will they escape from the meltdown? Or will they just disappear for good?

We worked out the timeline of the collapse and summarized its impact in our previous article The Collapse of LUNA. Today, we will focus on the latest development of Terra-powered projects after the meltdown, whether they are trying to meet the present challenge, and where they are heading.

Where are Terra-powered projects heading?

Astroport

Astroport is a leading DEX on Terra. As a Terra-exclusive project, the DEX is bound up with the Terra ecosystem, so it mainly trades the cryptos of Terra projects. As such, the TVL and trading volume of Astroport have been both hit hard by the crash.

In terms of TVL, according to Deflamama.com, on May 9, before UST de-pegged, Astroport’s TVL stood at around $1.26 billion but nosedived to $23 million on May 15, a drop of more than 50 times. The TVL drop indicates that LUNA and UST are not the only cryptos that crashed, and projects including Mirror, Anchor, and Astroport have also witnessed repeated slumps. As for the trading volume, data from Coingecko suggests that Astroport’s trading volume stood at $350 million on May 9, surged to $1 billion on May 11, and then plummeted to $16 million on May 13, 1/20 of the scale before the meltdown. Evidently, at the beginning of the UST de-peg, traders hoping to buy low and speculators planning to arbitrage through UST’s price mechanisms flocked to Terra, pushing up the trading volume of Astroport to a level much higher than usual in the first few days but soon driving it down into a bottomless pit.

Before the meltdown, the Astroport team never revealed themselves to the public. Yet after the collapse, they announced on May 11 that they hoped the members of the community could discuss where Astroport should go in the future and how the Terra ecosystem could be saved. As Astroport is tied together with Terra, liquidity is its best moat. Once the project loses liquidity, in the DEX sector with low technical barriers but intense competition, even if Astroport migrates to other public chains, its market prospects remain dim.

Anchor Protocol

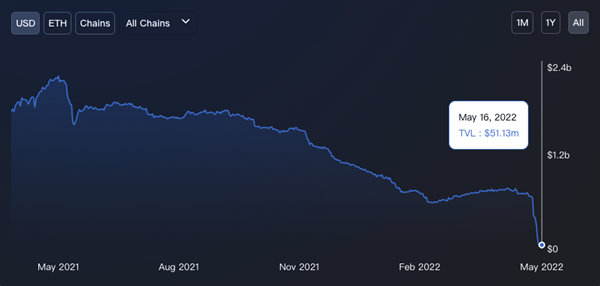

Anchor is the largest stablecoin lending project on Terra. It used to provide an APY as high as 20% for depositors through loan interests and staking rewards. In addition, depositors can also stake assets that include LUNA and ETH to borrow UST. As a key part of the Terra ecosystem, Anchor promises a stable ROI of about 20% and comes as one of the driving forces behind Terra’s soaring TVL.

Anchor’s interest rates became abnormal even before UST deviated from its peg: the borrowing interest rate went from positive to negative. Though Anchor lowered the interest rate to encourage users to stake assets like LUNA to borrow UST, the actual proportion of users borrowing remained low. As users all started to withdraw their UST deposits, Anchor witnessed the most straightforward impact of the UST de-peg. In addition, as the Luna price plummeted, the forced liquidation of bLuna continued, sending it into a downward spiral. Anchor’s TVL also fell off the cliff, dropping from 14 billion UST to 1.39 billion UST (as of May 16).

In terms of multi-chain deployment, apart from bLuna, Anchor also supports collaterals that include bETH, wasAVAX, bATOM, and bSOL. However, following the UST de-peg, users also started to redeem these collaterals on other chains. As of May 16, Anchor’s TCV (Total Collateral Value) of bETH, wasAVAX, bATOM, and bsol stood at $59.65 million, $5.05 million, $2.21 million, and $3,391, respectively. The massive withdrawal of assets indicates that investors are not confident in Anchor’s reboot.

After UST lost its peg, Anchor did not issue any immediate announcements to calm investors. Instead, it only tweeted that the blockchain had been suspended and called on users to stop interacting with Anchor. Without releasing any countermeasures, Anchor just asked users to wait for an update. Meanwhile, its official Discord server was locked, and users could only complain on Twitter. When it comes to the UST de-peg, given that the team behind Anchor is Terraform Labs, it might be too busy to consider the future prospect of Anchor for the moment being.

We believe that the problem with Anchor lies in the excessively low actual proportion of users borrowing. As most of the funds stay idle, Anchor has been consuming its reserves, which eventually led to the imbalance between borrowing and lending. In March, the Anchor community sought other solutions, such as adjusting the APY to a semi-dynamic interest rate, upgrading the protocol to Anchor v2, and allowing users to stake auto-compound derivatives. However, hit by the UST de-peg, Anchor’s attempt failed halfway through. If Anchor wishes to keep operating, it must first restore investor confidence and then improve the product logic to make ends meet.

Mirror Protocol

Mirror Protocol is a Terra-based decentralized platform where users can trade synthetic assets such as mTSLA that are pegged to Tesla’s stock price. Like Anchor, Mirror was also one of the major applications for UST to expand its coverage. Since the end of 2021, Mirror has got trapped in rumors of SEC investigations, and its TVL has gone downhill. The UST crash came as another major blow to Mirror. According to Mirror’s product mechanism, the protocol receives real-world stock prices through oracles and then changes the collateral ratio to guide synthetic assets on Mirror to track the prices of real-world assets. However, the synthetic assets on Mirror are all priced and traded in UST. Therefore, as UST deviates from its peg, the price of synthetic assets on Mirror also significantly deviated, with a premium of up to 40%.

Mirror is backed by Terraform Labs, which hasn’t released any information on Twitter since May 5, nor did it respond to the Terra/UST meltdown. Meanwhile, users have not been able to join its Discord channel since May 11. Due to regulatory pressure and the UST de-peg, Mirror might not make any big moves any time soon.

Mars Protocol

Other than Anchor, the Terra ecosystem also features another lending protocol called Mars, which is also a joint project led by Terraform Lab, Delphi Labs, and IDEO CoLab. Compared with Anchor, Mars aims to provide collateralized lending services for more tokens. To improve the utilization rate of loans, it innovatively provides functions similar to credit line for other protocols that grant credit to the protocol (such as Apollo, an Astroport-based revenue strategy platform).

After UST de-pegged, since most of the TVL of Mars comes from UST that users deposited during the Lockdrop stage, its TVL loss has been smaller compared with protocols that were heavily invested in LUNA (UST is now worth around $0.15). Moreover, as the protocol has not yet been fully launched, the bad debts generated by collateralized lending are limited. At the same time, when UST started to de-peg, the protocol immediately suspended the borrowing function and adopted urgent measures concerning existing UST liquidity providers. During Lockdrop, many users’ UST deposit was locked for 3 to 15 months. The Mars team unlocked such deposits through emergency multisig, which allowed users to withdraw their locked UST deposit freely. From proposal to execution, Mars moved quite fast.

Yet, it is noteworthy that unlocking UST, to some extent, reflects the project team’s lack of confidence in its reboot. This is the case because according to the official compensation program, Terra will allocate new LUNA tokens to UST holders, but Mars has allowed users to redeem UST tokens that should have been locked until next year (the average lock-up time), which also means it has given up the right to use new LUNA tokens allocated to the locked UST for a year or so. This dilutes the underlying value of MARS tokens, and also releases a signal that the team might be considering giving up or moving elsewhere.

Overall, the future of Mars, which is a lending protocol tied together with the Terra ecosystem, is full of uncertainties and challenges. Meanwhile, since the project team behind Mars is Terra Lab itself, we can basically rule out the possibility of migration to other chains. We should give credit for the quick decisions and swift actions taken by Mars during the meltdown. Compared with most Terra projects, Mars has done a great job in handling the crisis and calming and compensating the community.

Mars announced the suspension of borrowing services on May 10.

On May 13, Mars counted the bad debts and suggested that Delphi Lab, one of the teams behind the project, would pay off the debts.

On May 13, Mars unlocked the lockdrop UST.

Nexus Protocol

Nexus is a revenue strategy protocol. Its main strategy is based on Anchor’s bLUNA (a small part being bETH and wasAVAX). The core technology of Nexus is to use oracles to front-run Anchor’s liquidation mechanism, which allows users to mine with the maximum loan-to-value ratio, without the risk of forced liquidation.

As the UST de-peg directly zeroed out the value of LUNA, the TVL of Nexus’s bLUNA strategy is also approaching zero, and only bETH and wasAVAX still have a remaining TVL. Yet, since users panicked and ran away, the total TVL of Nexus has been depleted. According to Deflama.com, Nexus’s TVL once peaked at $153 million, and now only $500,000+ is left.

What’s worse, after UST broke its peg, the network of Terra also ran into some problems, and Nexus nodes were unable to sync with the mainnet, rendering the anti-liquidation mechanism invalid. As for the protocol strategies, approximately $600,000 of assets were liquidated. Immediately after the incident, the team conducted a technical analysis to investigate the reasons and drafted and proposed compensation plans.

For the Nexus protocol, the UST de-peg means it almost has to rebuild the project from scratch. However, considering Nexus’s innovative technology and design as well as the decent alternatives to the bottom-layer lending protocols like Anchor on other chains, the team could get redeployed on other chains and migrate its tokens. As Nexus is not a project developed by the Terra team, there is no need for it to keep operating within the Terra ecosystem. According to the team’s announcements, Nexus is still discussing its future possibilities, and it seems that the team still hopes to keep operating with no intention of settlement or dissolution.

On May 12, Nexus tweeted that “severe blockchain flooding” prevented its node from syncing with Terra.

On May 12, the day of the unexpected liquidation, Nexus released the cause of the incident and compensation plan.

On May 15, Nexus said that it was thinking about “what to do next” and was open to a wide range of possibilities.

Orion Money

Orion Money, a cross-chain stablecoin bank on Terra, converts stablecoins on different chains into wrapped assets to earn fixed stablecoin returns on Anchor. First launched on ETH, Orion Money was later deployed on Terra, BSC, and Polygon.

Orion Money’s TVL also fell off the cliff, dropping from nearly $75 million to $15.96 million. As of May 16, 4.95 million UST remains on Orion Money, and most other stablecoins have been completely withdrawn or almost so.

To their credit, the Orion Money team immediately tweeted after the UST de-peg to retain the confidence of investors, which indicates that they were already discussing how to resolve the crisis. Moreover, after UST broke its peg, the team has taken active moves to make sure that users can withdraw their stablecoins with minimal losses. On May 14, the team issued a document to help users withdraw UST faster and also reminded users of the potential airdrop of new LUNA. On Telegram, the members of the team disclosed that they had participated in Terra’s early investment and are now operating at a loss. They also said that the Orion reserved for the team had not been unlocked in the hope of restoring investor confidence.

Orion Money’s growth is based on Anchor, which makes the project an accessory for Anchor that only transfers stablecoins from other chains to Terra. This means a lack of technical barriers. If deployment on Anchor fails, Orion Money could only find another way out, shift the focus of the project, or seek redeployment on other chains that are similar to Anchor.

PRISM Protocol

PRISM Protocol was once considered Terraform Labs’ most innovative product. With PRISM, users can split their assets into yield and principal components. Right now, the protocol only supports the splitting of LUNA, which can be split into pLUNA (principal) and yLUNA (yield).

At the moment, the LUNA price is close to zero, and PRISM has also been hit hard. Data from DeFiLIama shows that PRISM’s TVL stood at nearly $500 million on May 7, but driven by LUNA’s plummet that began on May 8, coupled with the UST de-peg, plenty of users withdrew funds from the protocol, and its TVL kept falling. PRISM’s TVL now stands at only $87. Facing bleak prospects, the project is on the verge of dying.

PRISM, a project launched by Terraform Labs, said in its latest tweet on May 13: The team will also explore other opportunities in the coming weeks, including redeploying the protocol on any community-supported Terra forks or other public chains. At the same time, PRISM also encouraged community members to share their thoughts on Prism Forum (forum.prismprotocol.app). As of this writing, the PRISM team has not announced any further plans for future development.

To our community:

The last few days it’s been difficult to watch what’s happened on Terra & our heart goes out to the LUNAtics & Refractooors out there who’ve been affected.

We had only just completed our v1 launch and we were excited about starting to roll out our v2 product.

— PRISM (@prism_protocol) May 13, 2022

Pylon Protocol

Built on Anchor, a fixed-rate storage protocol, Pylon Protocol introduces a yields-based IDO launchpad and future payments-in-cashflow to DeFi. So far, it launched Pylon Gateway Launchpad, through which many Terra-powered projects completed their IDO. Pylon Gateway Launchpad also allows users to earn token rewards by staking UST to different pools, thereby participating in the IDO of different projects.

Pylon Protocol is the 5th project directly incubated by TerraForm Labs. Its unique IDO mechanism makes the protocol strongly dependent on UST and Anchor. Following UST’s shocking de-peg and the massive withdrawal of funds from Anchor, Pylon Protocol has also suffered a heavy blow. According to DeFiLIama, UST had a TVL of about $240 million before its de-peg. As the impact of Terra’s meltdown expanded, Pylon Protocol had to open up all pools and allow users to withdraw UST. As of now, Pylon Protocol’s TVL has plunged to only $5.4 million.

Pylon Protocol said in a long tweet posted on May 12 that the team is working on the issue of contract migration and that UST withdrawals have been opened up for all pools, but it has not updated any progress and specifics since then.

Original tweet:

Terra Name Service

Terra Name Service is a decentralized name service built on Terra. It turns long, random, unreadable Terra addresses into short, personalized, team-specific addresses (.UST).

The LUNA crash and the UST de-peg also affected Terra Name Service’s native token TNS, which slumped nearly 20 times since May 8 (from $0.2 to $0.014), and very few users have registered new domain names since then.

Terra Name Service tweeted on May 12 that it will announce the next step as soon as possible but has not updated any progress or remedial measures so far.

Conclusion

The death spiral of UST led to the total collapse of the entire Terra ecosystem. Do Kwon, Terra’s founder, announced the Terra Reconstruction Plan on May 14, hoping to protect the community and the developer ecosystem by forking Terra into a new chain. More specifically, 40% of the tokens to be issued by the new chain will go to Luna holders before the UST de-peg, 40% to UST holders at the time of the new network upgrade, 10% to LUNA holders before the chain halt, and 10% to the Community Pool to fund future development. At present, the proposal is still under discussion, and there are many disputes, including the direct doubt stated by Binance’s CEO CZ about whether the fork would bring any value to the new chain.

At the same time, Terra’s rivals are also hovering over its ecosystem. Ryan Wyatt, CEO of Polygon Studios, tweeted that he was working with certain Terra projects to help them migrate from Terra to Polygon and “will be putting capital and resources against these migrations to welcome the developers and their respective communities” to Polygon. On May 15, Juno Network, a Cosmos-based smart contract public chain that uses the same technical architecture as Terra, launched a proposal for starting the Terra Development Fund and plans to provide 1 million JUNO (worth more than $4 million) to help Terra projects migrate to Juno. Meanwhile, some other public chains (such as CSC) or communities have also shown a gesture of welcome for the migration of Terra projects.

On May 17, Do Kwon released another proposal on Twitter, hoping to fork Terra into a new chain that will no longer feature the stablecoin UST. The total amount of tokens to be issued by the new chain is 1 billion, which will be distributed pro-rata to LUNAUST holders, communities, and developers of the old chain. If the proposal got passed, the new chain would be launched on May 27. In any case, there is no doubt that Terra’s user base and funds, as well as the confidence in its ecosystem, have all suffered a heavy blow and will not recover any time soon.